����

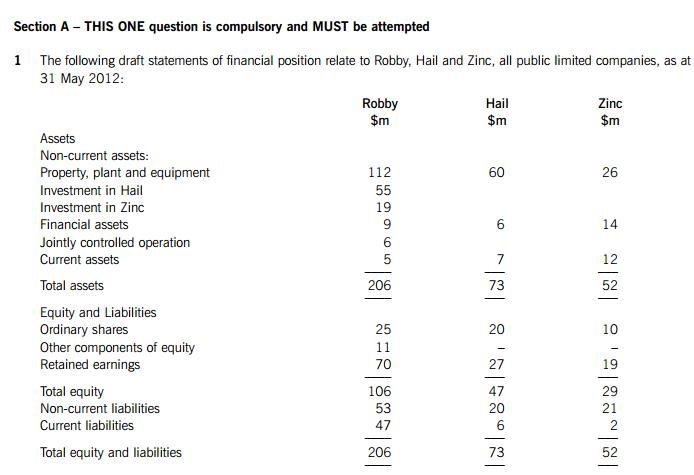

����The following information needs to be taken into account in the preparation of the group financial statements of Robby:

����(i) On 1 June 2010, Robby acquired 80% of the equity interests of Hail. The purchase consideration comprised

����cash of $50 million. Robby has treated the investment in Hail at fair value through other comprehensive income

����(OCI).

����A dividend received from Hail on 1 January 2012 of $2 million has similarly been credited to OCI.

����It is Robby��s policy to measure the non-controlling interest at fair value and this was $15 million on 1 June 2010.

����On 1 June 2010, the fair value of the identifiable net assets of Hail were $60 million and the retained earnings

����of Hail were $16 million. The excess of the fair value of the net assets is due to an increase in the value of

����non-depreciable land.

����(ii) On 1 June 2009, Robby acquired 5% of the ordinary shares of Zinc. Robby had treated this investment at fair

����value through profit or loss in the financial statements to 31 May 2011.

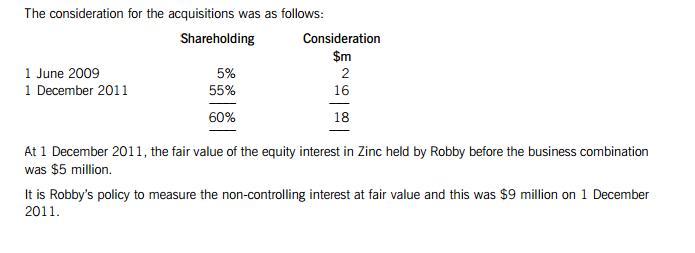

����On 1 December 2011, Robby acquired a further 55% of the ordinary shares of Zinc and gained control of the

����company

����

����The fair value of the identifiable net assets at 1 December 2011 of Zinc was $26 million, and the retained

����earnings were $15 million. The excess of the fair value of the net assets is due to an increase in the value of

����property, plant and equipment (PPE), which was provisional pending receipt of the final valuations. These

����valuations were received on 1 March 2012 and resulted in an additional increase of $3 million in the fair value

����of PPE at the date of acquisition. This increase does not affect the fair value of the non-controlling interest at

����acquisition. PPE is to be depreciated on the straight-line basis over a remaining period of five years.

����(iii) Robby has a 40% share of a joint operation, a natural gas station. Assets, liabilities, revenue and costs are

����apportioned on the basis of shareholding.

����The following information relates to the joint arrangement activities:

�����C The natural gas station cost $15 million to construct and was completed on 1 June 2011 and is to be

����dismantled at the end of its life of 10 years. The present value of this dismantling cost to the joint

����arrangement at 1 June 2011, using a discount rate of 5%, was $2 million.

�����C In the year, gas with a direct cost of $16 million was sold for $20 million. Additionally, the joint arrangement

����incurred operating costs of $0��5 million during the year.

����Robby has only contributed and accounted for its share of the construction cost, paying $6 million. The revenue

����and costs are receivable and payable by the other joint operator who settles amounts outstanding with Robby

����after the year end.

����(iv) Robby purchased PPE for $10 million on 1 June 2009. It has an expected useful life of 20 years and is

����depreciated on the straight-line method. On 31 May 2011, the PPE was revalued to $11 million. At 31 May

����2012, impairment indicators triggered an impairment review of the PPE. The recoverable amount of the PPE was

����$7��8 million. The only accounting entry posted for the year to 31 May 2012 was to account for the depreciation

����based on the revalued amount as at 31 May 2011. Robby��s accounting policy is to make a transfer of the excess

����depreciation arising on the revaluation of PPE.

����(v) Robby held a portfolio of trade receivables with a carrying amount of $4 million at 31 May 2012. At that date,

����the entity entered into a factoring agreement with a bank, whereby it transfers the receivables in exchange for

����$3��6 million in cash. Robby has agreed to reimburse the factor for any shortfall between the amount collected

����and $3��6 million. Once the receivables have been collected, any amounts above $3��6 million, less interest on

����this amount, will be repaid to Robby. Robby has derecognised the receivables and charged $0��4 million as a loss

����to profit or loss.

����(vi) Immediately prior to the year end, Robby sold land to a third party at a price of $16 million with an option to

����purchase the land back on 1 July 2012 for $16 million plus a premium of 3%. The market value of the land is

����$25 million on 31 May 2012 and the carrying amount was $12 million. Robby accounted for the sale,

����consequently eliminating the bank overdraft at 31 May 2012.

����Required:

����(a) Prepare a consolidated statement of financial position of the Robby Group at 31 May 2012 in accordance

����with Hong Kong Financial Reporting Standards. (35 marks)

��