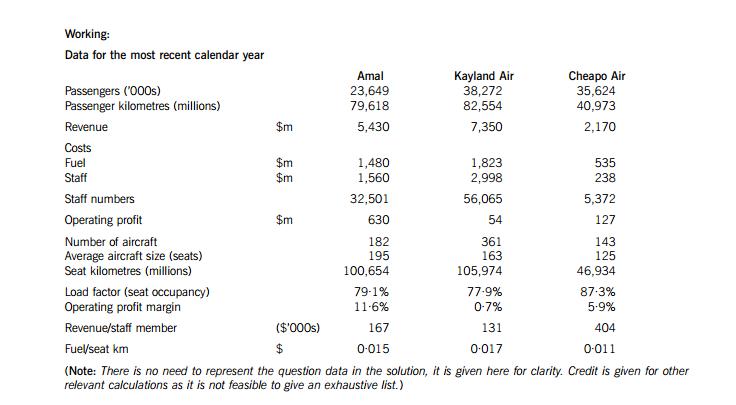

2 (a) The operating margin shows that overall Amal is being run efficiently. Also, the margin is relatively high which is to be

expected as Amal has a strategy of differentiation.

The load factor shows the utilisation of the expensive asset base of the companies and here, Cheapo is performing well ahead

of its rivals. This may be due to its pricing policy but it may be possible for Amal to review its own pricing policy along the

lines of Cheapo in order to boost the load factor. The danger of such a change to pricing policy is that it undermines the overall

strategy of Amal as a differentiator. So, it may be that load factor is a secondary rather than primary measure of performance.

The recent staff problems motivate looking at a measure of staff performance and workload. Amal is performing well ahead

of Kayland Air in generating revenue per staff member although it is much lower than Cheapo. This may be due to the power

of the staff in the publicly-owned Kayland Air and Cheapo offering a basic service with their use of outsourced staff.

Finally, the fuel costs are causing concern in the industry and it is noticeable that Cheapo is managing its fuel bills more

efficiently than either of the others. Amal should investigate possible savings by examining where Cheapo is sourcing its fuel,

what quality of fuel it uses and whether its aircraft are more fuel-efficient. (Note that fuel cost per seat kilometre has been

used rather than fuel cost per passenger kilometre since this reflects the fuel efficiency of the aircraft and does not confuse

this with the ability to fill the aircraft with passengers.)

(b) The performance prism has five facets which attempt to unify various methods of performance management into a coherent

whole. The facets are stakeholder satisfaction which then depends upon the other four facets of stakeholder contribution,

strategies, processes and capabilities. By taking a wider view and focusing on stakeholders, the prism model may help to

avoid performance measurement that is driven by internally-derived strategies.

Stakeholder satisfaction involves the identification of the important stakeholder groups and an understanding of their wants

and needs. At Amal, the key stakeholders appear to be:

– Finance providers (shareholders and lenders) who will want adequate returns for the risks that they take in allowing

management to use their funds;

– Customers who want the delivery of the premium service promised but who may resist the price margins that

accompany that product;

– Employees who want higher wages, job security and better working conditions; and

– Suppliers who are also key to delivering the new aircraft and the new website.

The stakeholder contributions identify what the organisation wants from its stakeholders.

– Amal will want shareholders (and lenders) to provide capital (possibly for the new aircraft) at a market price for the risk

taken and be committed to this investment for the time it takes to pay off;

– Amal will want customers who are loyal and profitable;

– Amal will want suppliers who are reliable (delivering on time is an issue for the website development) and support their

products with on-going technical improvements (for example, the new engine technology);

– Amal will need the commitment and cooperation of the employees if it is to deliver a premium standard service while

also, cutting costs.

The strategies are the paths that the organisation will follow in order to deliver stakeholder satisfaction. Amal has set a target

of reduction of overall costs by 14%. Two major categories are fuel and staff costs and part (a) has indicated possible routes

to improvement in these areas indicated by competitor activity. A gap analysis might yield ideas for further improvement by

identifying how much can be expected to be achieved through the existing squeeze on fuel and staff costs. An identification

of the cost drivers and an activity-based cost exercise would give a clearer understanding of general overhead costs. It is clear

that there may be a limit to the pressure that the staff will take before resorting to further costly strike action. Although it will

be important to measure the short term costs of industrial disputes with the long term benefit to profitability of reducing the

fixed staff cost base.

The processes are required if the strategies are to be executed. At Amal, it appears that the website project aims to streamline

existing processes. Cost per seat booked should fall as a result of this project. The project itself should be monitored against

budget as cost overruns are more likely when the project fails to meet its timetable. A larger exercise of business process

reengineering may be beneficial as large IT projects often offer the opportunity to remove redundant processes and redesign

the remaining ones. This would be a revolutionary programme of change but one that might well suit Amal as the staff appear

to have realised that there will be major change.

The capabilities are what are required in order to operate and improve the processes. The capabilities can be identified by an

audit of the strengths and weaknesses of the business. This can be achieved by considering the value chain and

understanding how value is generated by the linking of processes and skills in the business. It can also be achieved by using

18the McKinsey 7s model which identifies the hard elements as the strategy, organisational structure and systems alongside the

soft elements of shared values, style, staff and skills. Examples of performance measures in these areas would reflect the new

aircraft investment (e.g. return on new capital employed).

3 (a) There are a number of broad ways in which the implementation of Six Sigma improves quality in an organisation. These

include:

– an increased focus on customers illustrated at Thebe by the strategic need to improve customer service and the project

objective of improving customers’ bills;

– management decision-making being driven by data and facts not intuitions such as the use of customer satisfaction

scores or numbers of complaints as key performance measures;

– the identification of business processes’ improvement as key to success which is exemplified by the mapping of the

processes and then their redesign;

– the proactive involvement of management such as the CEO championing the billing improvement project. Six Sigma

depends on leadership which is provided by various experts who interact with the various Six Sigma projects which will

be improving processes in the organisation;

– the increased profile of quality issues and the increased knowledge of quality management that comes from the use of

different layers of trained experts in the project. There are green belts who will often be line managers, who in additional

to their normal work will lead Six Sigma projects. There are black belts who will exclusively specialise on Six Sigma and

lead specific projects and there are master black belts who are Six Sigma experts in statistical methods who consult

across several Six Sigma projects; and

– Six Sigma implementation requires collaboration across functional and divisional boundaries so bringing the focus of the

whole organisation to quality issues as illustrated at Thebe by the involvement of all the business units in the billing

project.

(b) The DMAIC process is as follows:

1. Define customer requirements/problem

Here the problem is the complaints on bills that result in customer dissatisfaction and delayed revenue receipt or

potential loss of business. Customer requirements can be divided into those that are the minimum that is acceptable

(e.g. billing errors are corrected), those that improve the customer’s service experience (e.g. billing corrections completed

swiftly) and those that go beyond the customer’s expectations (e.g. offering additional services as compensation). The

customers could be surveyed in order to identify if different customers have different needs (e.g. based on the three

business units).

2. Measure existing performance

The number of customer complaints or scores below a threshold level on customer surveys will have to be measured

and targets set (e.g. number of complaints per million bills issued or average time to resolve complaints). Measurement

should focus on areas where the customer will value improvement. A key issue at this point is ensuring that the

measurement system is reliable and this may require redesign of the existing customer survey forms/procedures.