7. Implement and monitor improvements

Management should perform a post-project review in order to identify if the improvement has achieved or exceeded its

goals and consider lessons that have been learned from the project.

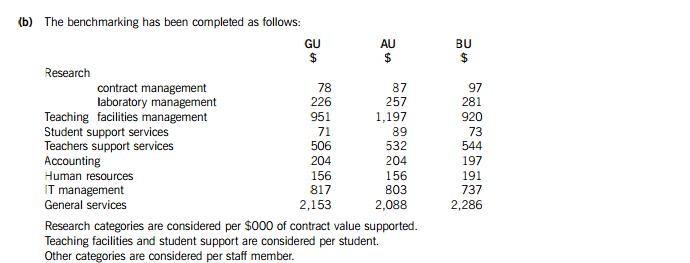

From the results, it can be seen that GU is best at controlling costs associated with research contracts and it has the highest

research funding ($185m). This may indicate that the government monitors such cost control and that GU should ensure its

continued good practice in this area. AU spends most per student on its teaching facilities and student support although it

has the smallest number of students. It might be expected that this would lead to higher student enrolment which may imply

that student enrolment is not significantly dependent on these factors. However, lower drop out rates and higher student pass

rates and future success in gaining employment may reflect the more expensive teaching environment at AU. These quality

measures are not being reflected in the benchmarking exercise.

In accounting services, all the universities perform broadly in line. BU has achieved a small 3·5% advantage over the others.

In human resources management, BU is 22% more costly which is surprising given the larger staff numbers at BU over which

to spread such a central cost.

In IT management, there is some variation of performance with BU costs being 10% lower than GU’s. These variations may

well be due to the subjects being taught (for example, universities that are more orientated to science and technology will

probably demand larger computing resources).

In general services, all the universities perform broadly in line. AU has achieved a small 3% advantage over GU.

It is necessary to give a warning about the difficulty of comparing the performance of the universities due to differences in

location and the mix of subjects taught and researched.

(Tutor note: the comments on accounting and general services are not significant and so not necessary in a good answer.

They are included for completeness.)

205 Performance measurement problems at Callisto

In a virtual organisation such as Callisto, performance measurement can cause difficulties due to the fact that key players in the

business processes and in the supply chain are not ‘on site’. Callisto has the problem of collecting and monitoring data about its

employees working from home and the outsourcing partners.

At Callisto, there is a reliance placed on information technology for handling these remote contacts. Collecting and monitoring

performance should therefore be done automatically as far as possible. A large database would be required that can be

automatically updated from the activities of the remote staff and suppliers. This will require the staff and supplier systems to be

compatible.

The employees can be required to use software supplied by Callisto and in fact, at Callisto, they use the internet to log in remotely

to Callisto’s common systems. Although this solution requires expenditure on hardware and software, it is within the control of

Callisto’s management. Even with reviews of system logs to identify the hours that staff spend logged in to the systems, there are

still the difficulty of measuring staff outputs in order to ensure their productivity. These outputs must be clearly defined by Callisto’s

managers, otherwise there will be disputes between staff and management. One further outstanding issue is the need to ensure

that such communication is over properly secured communication channels, especially if it contains customer or financial data.

The strategic partners, such as RLR, will have their own systems. A problem for Callisto is that there is disagreement over the

measurement of the key SLAs. In order to resolve such disputes, lengthy reconciliations between Callisto’s and RLR’s systems will

have to be undertaken otherwise there are no grounds for enforcement of the SLAs and the SLAs represent Callisto’s key control

over the relationship. The solution would be for the partners to agree a standard reporting format for all data that relates to the

SLAs which would remove the need for such reconciliations.

Finally, there is the problem that Callisto and the partner organisation may have differing objectives – the obvious conflict over price

between supplier and customer being one. However, at Callisto, this is being addressed by the use of detailed SLAs which both

organisations can use to develop performance measures such as inventory levels and delivery times.

Performance management problems at Callisto

The performance management of employees is complicated due to the inability of management to ‘look over their shoulder’ since

they are not present in the same building. However, employees will enjoy the advantages of home-working, such as lower

commuting times, more contact with family and greater flexibility in working hours. The disadvantages are the difficulties in

measuring outputs mentioned above and ensuring motivation and commitment. The motivation and commitment can be addressed

through suitable reward schemes which would have to be tied to agreed outputs and targets for each employee. Work could be

divided into projects where the outputs are more easily identified and pay and bonuses related to these.

The performance management issues of handling the strategic partners include:

– confidentiality where the partners will have access to commercially sensitive information about customers’ locations and

suppliers’ names and lead times;

– reliability where the partner is supplying a business critical role (as for RLR with Callisto) such that it would take considerable

time to replace such a relationship and affect customer service while this happened;

– relationship management where the interface between the organisations can create wasteful activity if there is not an

atmosphere of trust. At Callisto, this is illustrated by the problem of reconciliation of performance data;

– profit sharing where given the collaborative nature of the relationship and the difficulty of breaking it combine to imply that it

will be in the interest of both parties to negotiate a contract that is motivating and profitable for both sides. For Callisto, the

business aim is to increase volume and this will require customer loyalty so the quality of service is important.